Utilizing National Budgets or National Public Finance Systems

What is it?

Government budgets are at the core of sustainable development. The budget is the government’s most powerful economic tool to meet the needs of its people, especially those of poor and marginalized communities. Whichever SDG you may be interested in, the most well-intentioned public policy has little impact on that goal until it is matched with sufficient public resources to ensure its effective implementation.

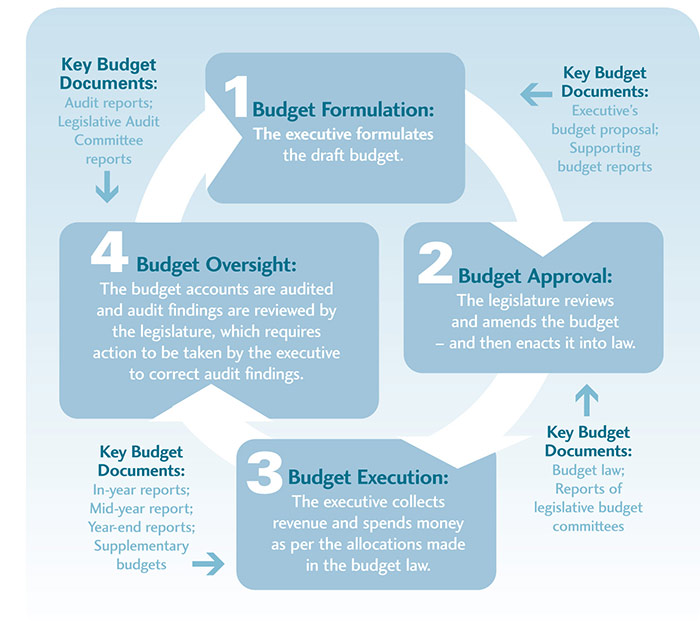

The government budget is a financial statement presenting the government’s proposed revenues and spending for a specific period of time, usually a year, which is often passed by the legislature, approved by the head of government, and presented by the finance minister to the nation. In most countries the budget process occurs in four stages, as shown below, and the various actors play different roles in each stage. While CSOs can have a big impact on budget decisions, implementation and outcomes, this impact is much greater when they work with other actors in the “accountability ecosystem” at different stages of the budget process (i.e. legislators, auditors, citizens, donors and the media).

Why is it important?

The decisions made in government budgets, and how those decisions are implemented on the ground, have a direct and transformative impact on people’s lives. Evidence shows that the best way to manage public funds efficiently and equitably is through budget systems that are transparent, inclusive, and monitored through strong, independent oversight institutions. On the other hand, lack of fiscal transparency and limited public participation and oversight undermine fiscal discipline, increase borrowing costs, undermine the efficiency of public services and create opportunities for corruption and other leakages.

When people have access to budget information, coupled with the skills and opportunities to participate in the budget process, the resulting engagement between government and citizens can lead to substantive improvements in governance and service delivery. As research shows, budget transparency, expenditure monitoring and accountability can contribute to increases in spending towards, and better results related to, development goals.

The 2030 Agenda and the Addis Ababa Action Agenda on financing for development (FfD) call for governments to report on their spending and progress towards the achievement of the SDGs. The 2030 Agenda specifically commits to building “effective, accountable and inclusive institutions at all levels,” and the Addis Ababa Action Agenda pledges to “increase transparency and equal participation in the budgeting process.” SDG indicator 16.6.1 focuses on the degree to which governments implement their budgets as planned, which is important for understanding whether governments are keeping their promises and delivering as planned on goods and services for citizens.

The 2017 session of the UN Economic and Social Council’s Forum on FfD Follow-up further recognized “the importance of better disaggregation of budget and expenditure data at the national and subnational levels, including by sex, to improve tracking of spending related to the Sustainable Development Goals and efforts to improve gender equality, accountability and transparency.” Finally, the Inter-Agency Task Force on Financing for Development emphasized that ‘stronger implementation of transparency and public participation in the budgeting process can improve the effectiveness of public finance’ (2017).

This is a critical time for civil society to engage in the budget process to further encourage governments to improve their planning, spending and reporting to meet the SDGs. How countries manage funds to deliver on the 2030 Agenda can have a transformative impact on people’s lives.

How can it be used?

CSOs play an important role in public budgeting. They can help improve budget policies by providing information on public needs and priorities through their connections with citizens and communities. Along with legislators, auditors, the media and the broader public, CSOs can also play an important role in holding the executive accountable for how it uses public resources.

When CSOs can combine in-depth knowledge of a policy issue such as health or education with solid knowledge of budgets and an effective advocacy strategy, they can positively influence policy decisions. Strengthening civil society’s ability to analyse budgets and participate effectively can play an integral role not only in policies and service delivery but also in constructing a more open and participatory democratic society.

CSOs can advocate for greater transparency and participation throughout the budget process and use available budget information to engage in the budget process and advocate for change. They can use the Open Budget Survey to assess budget transparency, participation and oversight, and advocate for the budget documents or information needed to track the SDGs.

There are opportunities for engagement in each phase of the budget process:

1. Budget formulation stage – CSOs can:

• Analyse pre-budget reports and publicize recommendations to try to influence the budget before final decisions have been made. Where CSOs do not have access to pre-budget statements or reports, they can draw on evidence generated from analyses of previous budgets to advocate for budget proposals.

• Gather information on the public’s needs and priorities for what should be in the budget and use this information, along with their own budget analysis and monitoring, to communicate these priorities to the executive. CSOs can draw on formal and informal communication channels to engage with executive officials.1

• Try to influence what goes into the Executive’s Budget Proposal (the government’s major statement on fiscal issues for the coming budget year) in various ways. This includes engaging with or in advisory committees and participating in public hearings or consultations.2

2. Budget approval stage

• As this process culminates in the enactment of the final budget law, when media attention is often at its greatest, CSOs can advocate for their issues. By providing independent analyses of the Executive’s Budget Proposal when information is in high demand, as it is during the approval process, and engaging in legislative deliberations, such as hearings and public policy councils, CSOs can inform the debate over the budget and influence its direction.3

• CSOs with technical skills can contribute to the approval process by analysing the revenue and expenditure policies being proposed and providing this analysis to legislators to help them more clearly understand the issues related to the budget and make better decisions. CSOs’ expert analyses and testimony can influence the debate, highlight important issues about the impact of budget proposals on poor or marginalized communities, and even build the capacity of legislatures to analyse budgets and improve the quality of budget hearings and reports.4

3. Budget execution stage – CSOs can:

• Advocate for the executive to issue public reports regularly on the status of revenues and expenditures during the year, so CSOs and other actors can monitor the flow of funds.

• Analyse whether governments execute budgets as planned – this is specifically highlighted in SDG indicator 16.6.1, but is relevant across all the SDGs. CSOs can draw on national budget documents, as well as Public Expenditure and Financial Accountability data and the World Bank’s BOOST data to check if governments are executing budgets as planned.

• Use in-year reports and mid-year reviews, which convey actual spending figures versus budget allocations, to monitor whether funds allocated to specific projects, such as a road or school, have actually been used for the intended purpose.

• Assess the quality of the spending by using budget information and physically verifying the end result of the project to see if the policy goals associated with the budget allocation are being met, and if government funds are being used effectively.5

4. Budget oversight – CSOs can:

• Use audit reports, if they are published in a timely manner, to assess how well or poorly the budget has been implemented, and potentially uncover fraud, unauthorized or unsubstantiated expenditures, or systemic weaknesses in financial management practices in public sector agencies.6

• Engage with oversight bodies to report on issues of public concern and help identify potential audits.

• Engage in participatory audits to collect, collate and distribute information and hold a public hearing or discussion on audit findings and recommendations, and follow up with responsible agencies or actors.

• Engage the media and other accountability actors to report on audit findings and recommendations.

A variety of legal, institutional and political factors will affect the extent to which civil society can engage in the budget process. Such elements can seriously hinder the efforts of national and local organizations attempting to participate in the debate on the use of public resources for the SDGs. Although the challenges are substantial, there are increasing demands pushing governments to open their budgets through information and participation to achieve sustainable development dividends.

Key Resources

• From Numbers to Nurses: Why Budget Transparency, Expenditure Monitoring, and Accountability are Vital to the Post-2015 Framework shows that budget transparency, expenditure monitoring and accountability can contribute to increases in spending towards, and better results related to, development goals. The brief draws on a vast array of case studies, as well as quantitative analysis of new data sets, to examine the relationship between transparency, monitoring, spending and outcomes.

• Open the Books: Why We Need to Open Budgets and Doors to Budgetary Engagement to Achieve the Sustainable Development Goals outlines practical things that can be done to ensure that public money is being raised and spent to deliver critical public services, implement development priorities and hold governments to account.

• Open Budgeting and Monitoring for the Sustainable Development Goals: A Country-level Perspective is a blog post written in support of the International Budget Partnership’s co-authored chapter and included in the Dag Hammarskjöld Foundation and United Nations Multi-Partner Trust Fund (MPTF) Office report Financing the UN Development System: Pathways to Reposition for Agenda 2030 (September 2017).

• Tracking Spending on the Sustainable Development Goals: What Have We Learned from the Millennium Development Goals? is a budget brief that explores good practices and lessons learned from monitoring of government budgets and expenditure on the Millennium Development Goals (MDGs), featuring summaries of case studies from eleven countries.

• Budgeting for a Greener Planet examines the formal accountability systems of four countries that will receive and manage substantial climate change funds (Bangladesh, India, Nepal and the Philippines). It serves as a tool in decision making and monitoring of the use of public funds for climate action and establishes a “climate finance accountability framework.”

• The Impacts of Fiscal Openness: A Review of the Evidence provides the first systematic review covering 38 empirical studies published between 1991 and early 2015, highlights gaps and sets out a research agenda that consists of: (a) disaggregating broad measures of budget transparency to uncover which specific disclosures are related to outcomes; (b) tracing causal mechanisms to connect fiscal openness interventions with ultimate impacts on human development; (c) investigating the relative effectiveness of alternative interventions; (d) examining the relationship between transparency and participation; and (e) clarifying the contextual conditions that support particular interventions.

• International Budget Partnership guides

• Financing for Development: Progress and Prospects 2018 report highlights basic information needed to track sector spending, budget implementation, and the goals and outcomes of spending.

• Our Money, Our Responsibility: A Citizens’ Guide to Monitoring Government Expenditures (IBP Guide, 2008).

• Guide to Transparency in Government Budget Reports: How Civil Society Can Use Budget Reports for Research and Advocacy (IBP Guide, 2011).

• The Role of Civil Society Organizations in Auditing and Public Finance Management (IBP Paper, 2005).

Case Study: Aligning Strategic Frameworks and Engaging Budget Officials

Tanzania: The implementation of the SDGs in Tanzania falls under the Five-Year Development Plan II (FYDP II) framework requiring local authorities to integrate the goals in their strategic plans. To ensure local authorities were familiar with the SDGs and aligned the FYDP II with their strategies, the Local Governance Working Group of Policy Forum, an NGO Network, developed a policy brief and engaged with the Parliamentary Committee for Administration and Local Government. The brief focused on the Ministry of Regional Administration and Local Government (PO-RALG), analysing budget allocation trends in relation to the implementation progress of SDGs, particularly Goal 3 on health and Goal 4 on education. The analysis further looks at the budget allocation trends within the Ministry of Health, Community Development, Gender, Elderly and Children (MoHCDEC), and the Ministry of Education, Science and Technology. Through their engagement, the Policy Forum was able to identify champions to push the SDG agenda during parliamentary discussions and also organize a strategic session with PO-RALG management to promote better SDG and FYDP II alignment. In addition, the network collaborated with the Tanzania Sustainable Development Platform to train PO-RALG management and other staff on the FYDP II, Agenda 2063, 2030 Agenda and the SDGs. As a result of such training and engagement, PO-RALG staff and councillors have a better understanding of the alignment between the SDGs and development plans, as well as the budget process, resource management and value for money.7